Asset Allocation Strategy for 2023

Risks and Opportunities in 2023. Rebalancing portfolios.

The past

From apr2020 until the last quarter of 2021, all assets were in a reflationary set-up, one in which policy support led to a boom in corporate profit, commodity prices and nominal growth. Corporate did their bit in squeezing extra margins. Bonds, equities, and real estate- all did very well in that period. Pretty much across the world.

Operating profit as % of sales of top 3k firms

By Q3 of 2021, it became evident to many of us that western policymakers were miscalculating inflation and sudden monetary policy support withdrawal was inevitable. (1) Post | LinkedIn

In the next few months, a sharp turn arrived resulting in a spike in yields. Bonds and equities bled. (1) Post | LinkedIn

Global policy tightening harmed the Indian macro in many ways. Our rates had to tighten prematurely and currency had to weaken. Remember our Governor was defending 6% on 10-year bonds a year ago and currency at 80 less than 6 months ago. Even though growth entered a slow lane - RBI’s reflex changed- prioritizing macro stability over growth. (1) Post | LinkedIn

The ongoing energy crisis caused wide CAD (Current account deficit). Our reserves dwindled. This led to the tightening of banking system liquidity. Deposit growth could not keep pace with credit growth. Acute tightness in money markets ensued. All of this was when India hadn’t even recovered fully. Our output (GDP) remains 10% below the pre-Covid trajectory. (1) Post | LinkedIn

In 2022, Nifty lost 5%, small caps 10%, S&P500 20% and US long bonds 30% (all in USD). Long USD cash was the best strategy last year.

The future ~ macro and policy

I think G2 (China and US) will do better than market expectations and Europe will do somewhat worse. In aggregate – the world economy will still be slowing through the year. The US will see its last rate hike in Feb. Following that, a protracted pause will unnerve markets that are accustomed to fast Fed pivots in every downturn. China’s re-opening is going to be good for commodities. It’s a strange point in a cycle when the two dominant economies (G2) and commodities will be doing alright whereas the rest of the world will be struggling with recession or sharp slowdown.

Indian growth will be in 5-6% lane. Disappointing for both pessimists and optimists. But for markets - more important is to note that Indian economic growth will rebalance. More in favour of poor India vs Rich India, rural India vs urban one. Our scooter economy will do better than the Car economy. Bear in mind that less than 10% own cars in India whereas 50% own bikes. Our growth will be less import intensive. So our current account deficit will improve.

RBI will likely hike more than market expectations. The Terminal Repo rate may be near 7% vs the market expectation of 6.5%. 2023’s will see sharply lower nominal growth. That will hurt corporate profits and government finances. Given the stress in money markets – RBI will be forced to pivot on liquidity. Short-term bond markets and credit markets may sizzle until then – giving an opportunity for investors.

Crude which got oversupplied during the last 2 months will rebalance and go back to deficit. China will add a million barrels a day to demand as it fully opens up in the next 3m. Price caps and the European embargo will reduce Russian supplies by half a million barrels a day. SPR refill will work as floor to crude. Likely higher crude through the year.

Our currency will likely depreciate by 3-5% due to high CAD (2-2.5%), low foreign flows and low rate differential (100+bp lower than average). The risk remains on the downside. But inferior payoff vs 2022 for that long USD trade.

On FII flows

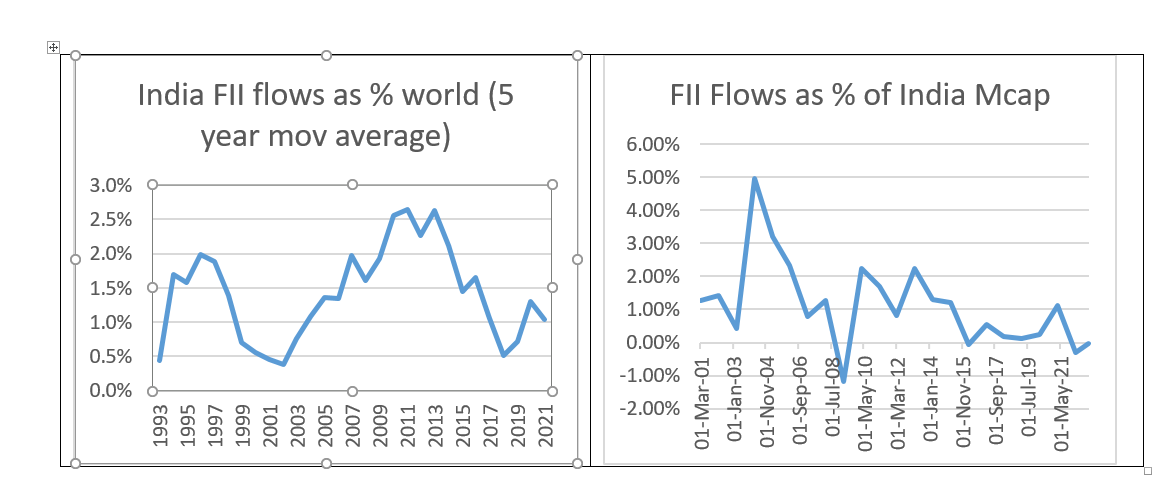

FIIs have been bringing in 1% worth of market cap on average over the past two decades. That number has dropped to nearly 0.25% over the past 5 years. Don’t expect significantly more than that in years to come.

Structurally, FII flows are about the savings of a small group of people. A 45-65 age group of developed markets. These folks are big savers as well as risk-takers. In most DMs - and more specifically in the US, this group’s size will begin shrinking over many years. It will be smaller by 3% in a decade.

Our market shares in ex-OECD global flows (60-70bn) is about 15%. Even in the mid90s, we had a similar share. Of the total global flows- our share is 1%. This share peaked in 2007 at 2.7%. Net net, FIIs aren’t a significant force to reckon with.

On Mutual fund flows

As % of GDP, MFs have been getting about 0.9% of market cap (since Modi 1.0), ex ETF about 0.6%. The last two years have been more buoyant at nearly 1%.

Its important to note that fund flows tend to be elastic to rates. Given the significant SIP accretion and the mainstreaming of MFs in India, it is doubtful that fund flows would reverse but they will certainly cool off. Something similar happened in fy19 over fy18 when high rates led to a significant reduction of mutual fund flows.

In aggregate – India’s equities flows by FII + MFs are already at .75% of market cap vs past decade’s average at 1.3%. FIIs contribution will be higher over the next 12m whereas mutual funds will be lower. The trade is to stick to the common portfolio of MFs and FIIs. Since small and midcaps tend to do well when MFs flows are buoyant and rates are low – the set up continues to be weak for such firms’ business prospects and valuations. (1) Post | LinkedIn

Corporate earnings outlook:

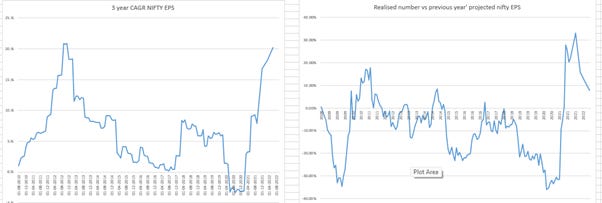

The trailing 12-month NIFTY EPS is 825. Next year, it is predicted to rise by 20%. Analysts overestimated profit growth by 9% on average over the prior decade, are they doing the same yet again?

A few points to ponder here. One, Indian earnings have been quite strong as the three-year CAGR of Nifty earnings is equivalent to the earnings rebound from the trough of 2009. And this is a phenomenal performance given that earnings did not decline as much as they did in 2009 (28% drop). Among the wider universe of 3k odd ex-financial enterprises, one can already observe weakness where operating margins shrank in the September quarter. Tight liquidity will soon begin to exert pressure on credit growth. Nominal growth is unlikely to be more than 12% in 2023. In that setup - the expected Nifty EPS growth will perhaps be as much as the Nominal GDP growth only. Maybe a little more given. But disappointing nonetheless. (1) Post | LinkedIn

Indian equities valuation:

Indian markets are valuing trailing profits at 22 times. Markets are trading at about 19.5 odd times the forecasted earnings. India is one of the very few markets that is trading at a premium to pre-Covid valuation. Even though interest rates were lower pre-Covid, our markets were trading at 18 times. Compare this to the United States at 17 times, which is 5% lower than pre-Covid levels. We are trading at a 70% premium to EM, compared to the historical average of 40%.

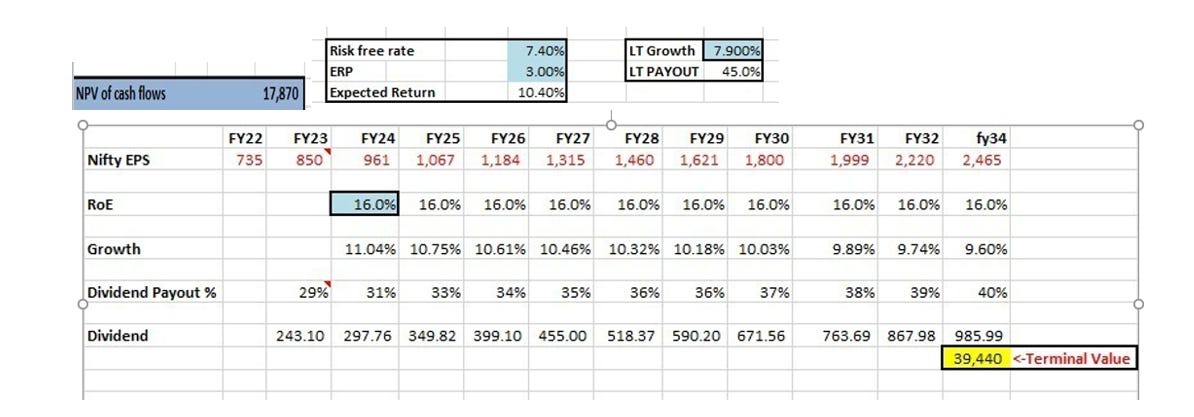

Following assumptions of 16% ROE for corporate (2% higher than the past few years’ averages), 30% dividend distribution rising to 40% over the next decade, terminal growth near 8% (long bond +50bp), long-term dividend distribution of 45% (similar to the US), current risk-free at 7.4%, the available equity risk premium is just under 3%.

Is this sufficient? The last decade provided 5%+ above bonds, while the excess delivered over two decades is 9%. The interesting thing is that we received 5% over and above bonds when rates were near at their peak a decade ago and 9%+ excess when they were at their all-time low two decades ago. Interest rates at the moment are just in the middle – neither too high nor too low. No one knows what markets expect, but if the previous 1-2 decades are any indicator for the expected risk premium, markets may be mispricing it.

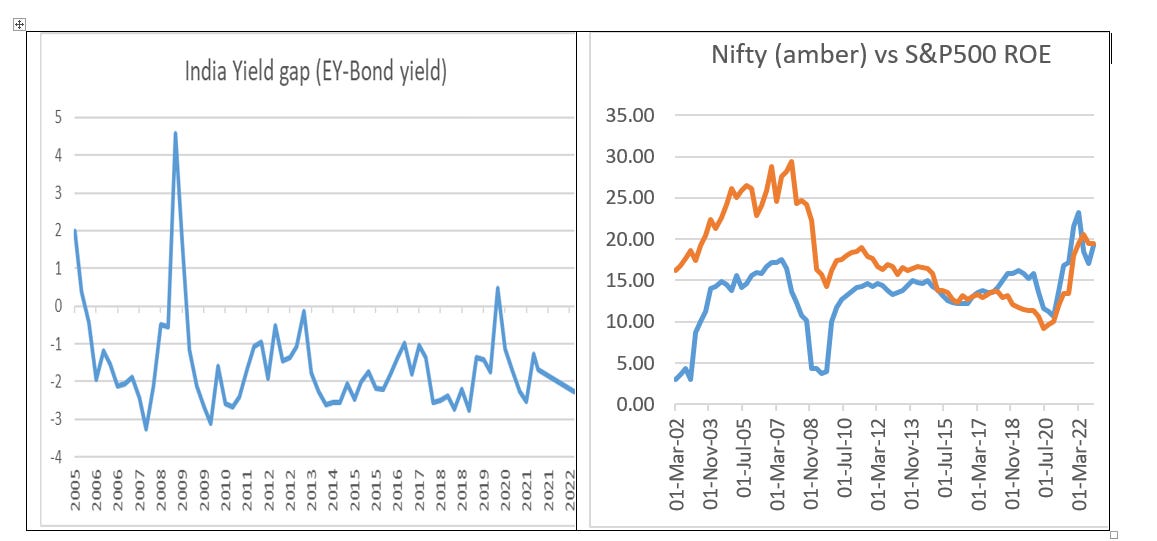

Another way to compare bonds vs equities is to gauge the excess return of Indian equities over bonds on a three-year rolling basis. At 12%, it has been an exceptional performance. If history is a guide, current outperformance will mean revert. (1) Post | LinkedIn

One more point. Indian enterprises used to have significantly greater ROEs than their US firms. No more. Through the past three years, which were outstanding in terms of business profitability, NIFTY ROEs averaged 15%. People in love with small firms – must take note of abysmal ROEs of them over past decade (~5%). Not sure – the macro set up has changed meaningfully to expect higher ROEs by them. (1) Post | LinkedIn

Asset allocation and bets

Some small finance banks are offering 9% on 1-2 year deposits. PSU banks deposit 8%+. Most short-term fund yields are close to 8%. AA-centric portfolios will yield near 10%. So opportunities galore in fixed income. Add them. Don’t sit on cash now.

Since US tech stocks have had a decent liquidation + valuations are cheap. So it’s time to start adding US tech ETFs in India. Earnings will most certainly be lower in the next quarters, although recent layoffs will enhance margins. Lower rates will aid valuations. Do a programmed buying over next few months if you are used to SIP strategies.

Long US rates will likely rally as the market begins to sight lower inflation. Lots of passive flows will be directed towards bonds. 2-5 year Govt and investment-grade bond yields will be lower in a year.

I must highlight that US bonds are trading at cheaper valuations as the gap between US earning yield and TIPs has actually narrowed over the past year. If you were to simply choose between US bonds and equities – the former is still a better risk-adjusted trade.

Indian equities remain moderately pricey, but not prohibitively so. Another year of a barren market awaits. The risk premiums are not sufficient to be overweight equities. Use the present market setup to diversify your portfolios away from India or add fixed income.

Small & mid-caps will likely struggle. Low nominal growth squeezes such firms’ pricing power. Tight liquidity reduces their access to capital. All in a bad macro set-up for such firms continue. Same as last year.

Stay with large firms and if you find no one better alternative – be in Index. The peak ROTA and NIMs for banks are in. Small banks and NBFCs will struggle for funding seeing their margin compress more remarkably. IT and commodities will likely surprise positively relative to pessimistic expectations.

If the global economy doesn’t sink into recession, peak rates will likely be higher. If it does – a major risk-off will ensue, and given our high CAD – RBI reflex may still be for higher rates in the near term. The former is more likely. All in-long rates are still not suitable for investors. Treasuries may stick to short-term bond funds instead of adding duration funds to their portfolios. (1) Post | LinkedIn

*forgive me for mis-spellings and grammatical mistakes. I know there are too many of them. Plus in the ERP sheet - I didn’t correct for today’s nifty level. Too lazy to re-do it. But you get the gist. don’t you? Happy new year! May you be well :)

Good write-up Maneesh, wishing you a happy new year!!

hi Maneesh, wish you also a very happy new year 2023 !

i liked your write-up. esp the FII and DII MF flows as a %age of mcap- i dont remember seeing that elsewhere.

being a bond mkt man for so many years, i suppose you are more comfortable with that mkt ? I wonder if you have done a backtest, for changing asset allocation between bonds and equities based on some of the valuation parameters mentioned ?

typically equity guy always insist that long only equity for long term gives best returns. is that really so ? given that debt mkt (in India at least) has given healthy nominal returns in many phases, i am inclined to believe active asset allocation wud have given better outcomes, at least in the past 25 yrs. wud love to hear your views / analysis on this. cheers n regds.